Protecting Your Workforce: Occupational Accident

As the economy and the independent workforce continue to expand, many businesses are rethinking how they protect the workers who help power their operations. Firms specializing in areas including trucking and delivery, staffing, and healthcare are turning to new strategies. Occupational Accident coverage has emerged as a flexible, cost-effective strategy for the independent contractor and 1099 workforce.

Strategic Advantage of Occupational Accident Insurance

For organizations that rely on contract labor, Occupational Accident (OccAcc) can be a vital safety net. Unlike Workers’ Compensation, OccAcc coverage is optional and can be 20-30% more cost-effective, making it an attractive risk management option for organizations.

As this coverage is not bound by rigid state mandates, coverage can be tailored. Generally, policies include coverage for medical expenses, a portion of lost wages, and death benefits up to the policy limits. For companies seeking a practical and scalable way to support their independent workforce while managing costs, Occupational Accident insurance can serve as a strategic complement to a broader risk management program.

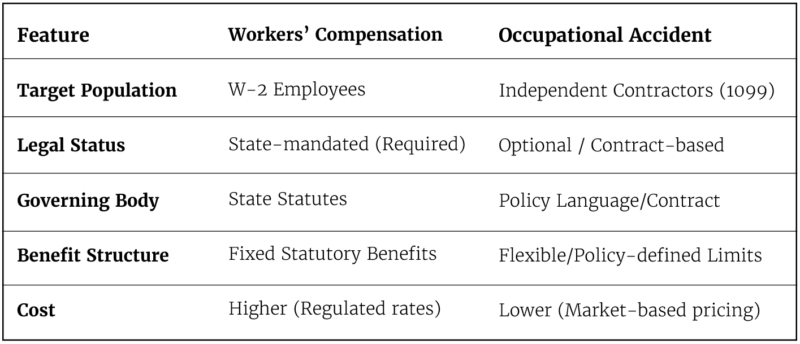

Key Differences: At a Glance

How does Occupational Accident Insurance Differ from Workers’ Compensation?

For businesses relying on independent contractors, understanding the difference between Occupational Accident insurance and Workers’ Compensation is essential. While both provide protection for work-related injuries, they are built for different employment relationships and operate in vastly different ways.

Nuances of Coverage

Statutory vs Contractual Requirements

Workers’ Compensation is a state-mandated program that covers employees (W-2 workers). In most states, employers are legally required to carry Workers’ Compensation if they have employees, subject to state statute requirements.

Occupational Accident insurance, on the other hand, is designed specifically for independent contractors (1099 workers). Because contractors are not considered employees, they are generally not eligible for Workers’ Compensation benefits, making Occupational Accident coverage a practical alternative.

Benefit Scope

Workers’ Compensation is required by state law in nearly every state, with benefits and rules governed by statute. Workers’ Compensation provides statutory benefits, which typically include:

- Medical expenses

- A defined percentage of lost wages

- Disability benefits

- Death benefits

OccAcc insurance is optional. It is a contract-based policy, meaning benefits, limits, and definitions are determined by the policy language rather than state statute. This flexibility allows businesses to tailor coverage to their operational needs.

OccAcc policies generally cover:

- Medical expenses

- A portion of lost wages

- Accidental death and dismemberment benefits

However, benefits are subject to policy limits chosen vs statutes and may vary by plan design.

Classification Impact

One critical distinction is classification of workers. Workers’ Compensation applies to employees, and misclassifying employees as independent contractors can lead to significant legal and financial consequences. OccAcc insurance does not replace the need for proper classification, rather it complements a contractor-based workforce model.

Cost Considerations

OccAcc insurance can often cost less than Workers’ Compensation (many times 20–30% less) because it is not regulated in the same way. For companies with a large 1099 workforce, this can represent meaningful cost savings.

Summary

For industries heavy on 1099 labor, the choice between Workers’ Compensation and Occupational Accident insurance isn’t just about cost—it’s about compliance and strategy. By understanding these distinctions, businesses can implement a risk management program that protects their bottom line while ensuring their workforce remains resilient and supported.